The sign went up on a Thursday morning in late February — a laminated sheet of paper taped to the drive-thru window at Copper Cup Coffee on Regent Street, the kind of note you read once and then read again because you don’t quite believe it the first time. “Effective March 1, 2026, Copper Cup Coffee will be permanently closing.” Eleven words. Three years of someone’s savings, gone.

I’ve been watching Sudbury’s independent food and beverage scene closely enough that the closure didn’t surprise me — but the timing did. February is brutal in Northern Ontario even in a good year, and 2026 has been anything but. What caught my attention wasn’t the closure itself. It was how fast the comment section filled up with people saying “I knew this was coming” — and how none of them could clearly explain why they knew.

So let me try to explain it.

The Drive-Thru Model Was Never Built for This Geography

Here’s the thing that gets glossed over in most coverage of small business closures in the North: the drive-thru coffee model in a mid-size Northern Ontario city operates on fundamentally different math than the same model in Mississauga or even Ottawa. Sudbury’s population hovers around 165,000 in the greater area, but that number is spread across a footprint that would swallow most southern Ontario cities whole. The city’s amalgamation in 2001 stitched together communities like Capreol, Lively, and Garson that are separated by 20 to 40 minutes of actual driving — not suburban sprawl driving, but two-lane highway driving in -30°C weather.

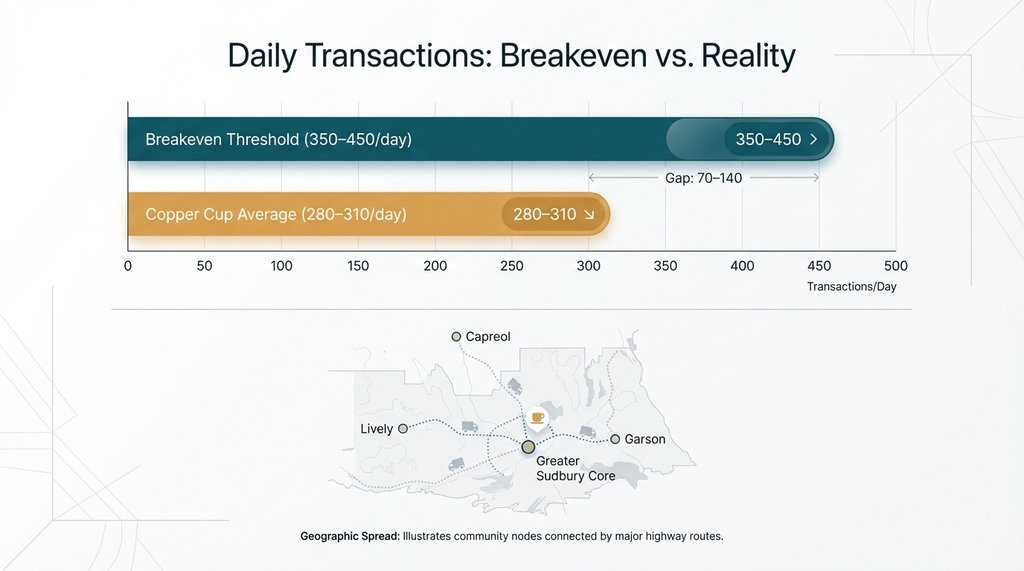

An independent drive-thru in that environment needs somewhere between 350 and 450 transactions per day to hit breakeven, based on the unit economics that operators in the region have shared with me over the past two years. Copper Cup, from what I’ve been told by someone who worked there through 2025, was consistently hitting 280 to 310 on weekdays by last fall. That’s not a failing business in the catastrophic sense — it’s a business that never quite crossed the threshold, grinding slowly toward a cliff it could see but couldn’t sprint away from.

The drive-thru format was chosen, in part, because the owners watched Tim Hortons and a local competitor called Perk & Pour do strong numbers on similar lots. What the benchmarking missed was that both of those operations had been on their locations for over a decade. In Northern Ontario, regulars aren’t won — they’re inherited. You don’t build a coffee loyalty customer base in 36 months the way you might in a high-turnover urban neighbourhood. The customer who stops at the same window every morning at 7:14 on the way to the Finlandia Village or up toward the Maley Drive extension has been doing that for eight years and will keep doing it for eight more, unless something forces a change. Copper Cup was asking people to change, and Northern Ontario customers are, in my experience, among the most route-loyal in the country.

What 2025 Actually Did to the Cost Side

I want to push back on the narrative that’s already forming online — the one that says “it’s all inflation” and leaves it there. Inflation is real, but it’s a lazy explanation that papers over where the actual damage happened.

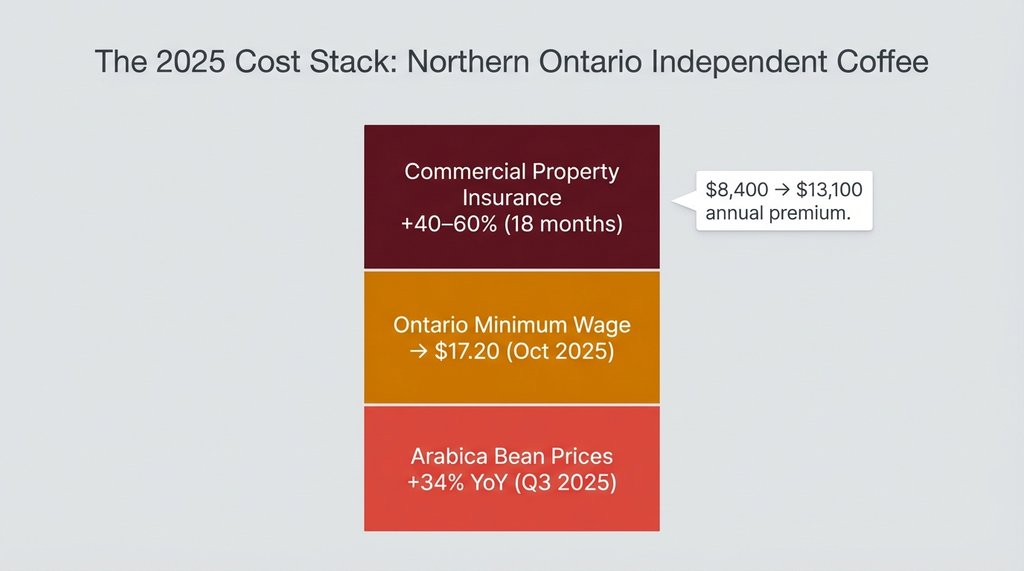

The Ontario minimum wage increase to $17.20 in October 2024 wasn’t the killer on its own. The killer was the combination: minimum wage up, coffee bean commodity prices that spiked roughly 34% year-over-year by Q3 2025 (arabica futures were sitting near record highs through most of the summer), and a specific regional problem that doesn’t show up in any national cost-of-doing-business report — Northern Ontario’s commercial property insurance premiums.

I looked at this specifically because an operator in Timmins mentioned it to me offhand in September. Commercial property insurance for a food service location with a drive-thru lane in Northeastern Ontario has gone up between 40% and 60% for many independents over the past 18 months. The reason insurers give, when they give one at all, involves a combination of extreme weather frequency, the age of commercial building stock in northern cities, and — this one stunned me — the reclassification of certain flood and ice-event risks following two consecutive bad springs on the Sudbury basin. One operator told me his annual premium went from $8,400 to $13,100 between renewals. That’s $4,700 a year that has to come from somewhere, and in a thin-margin coffee operation, it doesn’t come from anywhere except the owner’s salary, which was already doing the work of subsidizing the business.

The Franchise vs. Independent Split Is Getting Wider, Not Narrower

This is where the Copper Cup story stops being about one coffee shop and starts being about something structural.

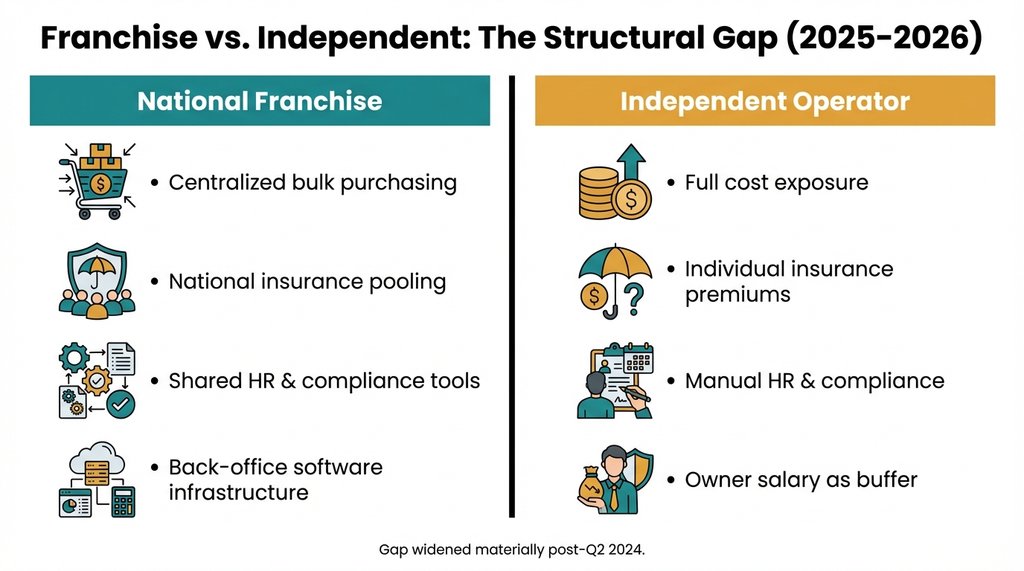

National franchise operations — and I mean specifically Tim Hortons, but also the aggressive westward push of Second Cup’s reconstituted franchise model — are able to absorb input cost shocks in ways that independent operators cannot, and the gap has grown measurably since 2023. It’s not just corporate buying power on beans. Franchise networks in 2025 and 2026 are accessing shared back-office infrastructure, centralized HR compliance tools, and national insurance pools that effectively cap the kind of premium spikes independents are eating whole. When a Tim Hortons franchisee in New Sudbury sees their insurance bill climb, that increase is partially socialized across the network. When Copper Cup’s owner saw hers climb, it came entirely out of her household.

I’ve spoken with three independent coffee operators in Northern Ontario in the past six months — one in Sudbury, one in North Bay, one in Sault Ste. Marie — and all three named the same inflection point: sometime in the second half of 2024, the structural advantages of the franchise model stopped being theoretical and started showing up in the actual monthly P&L comparison. Before that, a sharp independent with a strong local brand could compete on quality and community loyalty. After that, the math started winning and the loyalty stopped mattering.

The Sault operator put it this way: “I used to think I was competing against Tim’s on coffee. Now I’m competing against Tim’s on accounting software and their group benefits plan.” That’s not a fight any independent can win, and it’s producing a slow, grinding wave of closures that doesn’t look dramatic in any single month but is rewriting the commercial landscape of every Northern Ontario city street by street.

The Pattern Sudbury Residents Are Misreading

The common read on a closure like this is: bad location, or the coffee wasn’t good enough, or the owners didn’t work hard enough. That framing is wrong in a way that matters.

Regent Street is not a bad location. Copper Cup’s product was, by most accounts I’ve heard, well above average. The owners were working open to close for most of the first year. The closure is happening because a set of structural conditions that were marginal in 2022 became untenable in 2026, and those conditions are not specific to this one business. They’re specific to independent food service in mid-size Northern Ontario cities, operating in a post-2024 cost environment, competing against franchise infrastructure they can’t replicate, serving a customer base that is loyal but not abundant enough to absorb the math.

Downtown Sudbury lost four independent food and beverage operations in 2025 — a ramen shop on Elgin, two café-bakery hybrids, and a juice bar that had been there since 2019. The BIA numbers for Q4 2025 showed commercial vacancy on Elgin and Durham Streets at just under 19%, which is the highest it’s been since the 2015 nickel price collapse hit the local economy. That comparison is instructive. The 2015 closures were demand-side — people had less money to spend. The current closures are cost-side — the economics of running the business have shifted beneath operators who built their models on 2019 and 2021 assumptions.

That distinction matters enormously for anyone thinking about what the recovery looks like, if there is one. Demand-side contractions can reverse when commodity prices recover or employment improves. Cost-side structural gaps between franchise and independent operations don’t close on their own. They require either a policy intervention — there’s been some talk at the municipal level in Greater Sudbury about a small business utility rate class and a commercial insurance advocacy program, though nothing formalized as of early 2026 — or a fundamental rethink of what an independent food service business can sustainably look like in this geography and at this cost basis.

What Nobody Wants to Say Out Loud

The honest version of this conversation, which I’ve had pieces of with operators across the region over the past year, is that the independent drive-thru model in Northern Ontario’s mid-size cities is probably not viable anymore at the scale it was being attempted. A 400-square-foot drive-thru window with two or three staff, serving a catchment area of 12,000 to 18,000 people, built on 2021 lease rates and 2020 insurance assumptions — that specific business model has a structural problem that passion and good coffee cannot solve.

What might work, and what I’ve seen survive while others have closed, is a hybrid format: smaller footprint, higher margin add-ons, some kind of weekday anchor (catering contracts, office delivery routes, wholesale to a local hotel). One operator in New Liskeard has been quietly running a drive-thru coffee window that’s attached to a small wholesale bean operation and a Tuesday-Thursday catering route to three mining camp offices, and she told me last November that the wholesale and catering revenue is what pays her rent. The drive-thru covers labor. That’s a fundamentally different model than what most people picture when they think “local coffee shop (or even bars that serve specialty coffee),” and it requires a level of operational complexity that not every entrepreneur signed up for.

The Copper Cup closure is painful, and it’s real, and the people who are mourning it on Facebook are right to mourn it. But the mourning should be accompanied by a clearer-eyed understanding of why it happened — because the same pressures are sitting on every other independent food service operator in Greater Sudbury right now, and the ones that make it through 2026 will be the ones who figured out, one way or another, how to stop competing on the terms the franchise model has already won.

1 thought on “Sudbury Drive-Thru Coffee Closure: 2026 Business Trend”